|

RIYADH, Saudi Arabia, May 1, 2024/ — The Islamic Development Bank Group Business Forum (THIQAH) (www.IDBGBF.org) and the World Association of Investment Promotion Agencies (WAIPA) have recently signed a Memorandum of Understanding (MoU) aimed at fostering collaboration to promote business and investment opportunities on a global scale. The signing ceremony, held in Jeddah, Saudi Arabia, signifies a strategic alliance between THIQAH and WAIPA, two prominent entities dedicated to facilitating economic growth and investment promotion. Under the MoU, THIQAH and WAIPA commit to cooperating through various initiatives such as promoting investment opportunities, organizing international business-related events, and facilitating access to information and resources for potential investors. The agreement underscores the shared vision of both organizations to enhance economic development and create mutually beneficial partnerships. Distributed by APO Group on behalf of Islamic Development Bank Group Business Forum (THIQAH).

Contact Us: Email: THIQAH@isdb.org |

Category: Banking & Fianace

-

Memorandum of Understanding Signed Between The Islamic Development Bank Group Business Forum (THIQAH) and World Association of Investment Promotion Agencies (WAIPA) to Boost Business and Investment Opportunities

-

18th Islamic Development Bank (IsDB) Global Forum to Explore Innovation, Entrepreneurship, and Leadership in Islamic Finance

JEDDAH, Saudi Arabia, April 21, 2024/ — The Islamic Development Bank (IsDB) Institute (https://IsDBInstitute.org/) is pleased to announce the 18th edition of the IsDB Global Forum on Islamic Finance to be held in Riyadh, Kingdom of Saudi Arabia, on 28 April 2024, in conjunction with the IsDB Group Annual Meetings and Golden Jubilee Celebration.

Organized annually as a flagship side event of the Annual Meetings, this year’s Forum will bring together thought leaders, policymakers, financial experts, and other stakeholders in the Islamic finance industry to deliberate on innovative tools to foster sustainable development.

Under the theme “Innovation, Entrepreneurship, and Leadership in Islamic Finance”, the forum will have keynote speeches by H.E. Dr. Muhammad Al Jasser, Chairman of the IsDB Group; H.E. Dr. Stephen Groff, Governor of the Saudi National Development Fund; and Engineer Mutlaq H. Al-Morished, CEO, Tasnee Corporation.

The forum will witness the award presentation to the winner of the 2024 IsDB Prize for Impactful Achievement in Islamic Economics. Professor Mehmet Asutay, a professor of Middle Eastern and Islamic Political Economy & Finance at Durham University, won the prize in recognition of his significant and influential contributions to the field of Islamic economics and finance.

Subsequently, the Forum will have two sessions. The first is a panel that aims to explore the pivotal role of entrepreneurship in advancing sustainable development, particularly within the Islamic finance paradigm.

Panelists for the session are Mr. Mohammad Abdulhameed Al-Mubarak, CEO of Madinah Knowledge Economic City; Dr. Zeger Degraeve, Executive Dean of Prince Mohammed Bin Salman College (MBSC); Mr. Morrad Irsane, CEO and Founder of TAKADAO; and Dr. Sami Al-Suwailem, Acting Director General of the IsDB Institute.

The second session will showcase the Smart Stabilization System, a patent-pending algorithm to enhance stability in financial markets, being developed by the IsDB Institute and implemented by the blockchain company SettleMint. The discussants will be Mr. Matthew Van Niekerk, Founder & CEO of SettleMint, and Dr. Hilal Houssain, Associate Manager of Knowledge Solutions Team, IsDBI.

The Forum will also feature the launching of a new IsDBI report titled “Catalyzing Social Entrepreneurship through Islamic Finance”, which explores the potential of Islamic finance to support social entrepreneurship and impact investing.

The IsDB Global Forum on Islamic Finance is an annual high-level forum initiated in 2006 as a platform for strategic policy dialogue on knowledge and innovation in Islamic finance and development.

Distributed by APO Group on behalf of Islamic Development Bank Institute (IsDBI).Media contact:

Habeeb Idris Pindiga

Associate Manager, Knowledge Horizons

hpindiga@isdb.orgFor more information, visit the 2024 IsDB Group Annual Meetings website (https://IsDM-AM.org/) or IsDBI media platforms:

-

West Africa’s franc: is time up for the colonial currency?

By: Kai Koddenbrock, Bard College Berlin

First Published,April 8,Africa Edition/The Conversation

At no point in history has the CFA franc – the name of a colonial currency used in west and central African countries belonging to the franc zone – been closer to its demise.

Senegal has overwhelmingly voted for leftwing Pastef candidate Bassirou Diomaye Faye (and his former party leader Ousmane Sonko) while the coup governments in Mali, Burkina Faso and Niger have been talking about leaving the CFA franc for some time.

Senegal under outgoing president Macky Sall was a pillar of the longstanding French attempt to remain influential among its former colonies, often named “Francafrique”. Now newly elected Faye, under the moniker of “Left Panafricanism”, has vowed to make his country more sovereign in food, energy and finance.

Never before have four west African governments, including one of the regional leaders, Senegal, been simultaneously eager and ready to get out of the neo-colonial stranglehold of the CFA franc.

The CFA franc zone was founded by then colonial power France after the second world war. Its aim was to ensure a continuously cheap influx of resources into France.

The zone is divided into two. The west African CFA franc zone has eight members: Mali, Niger, Burkina Faso, Senegal, Côte d’Ivoire, Benin, Togo and Guinea-Bissau. The central African zone has six: Cameroon, Gabon, Republic of Congo, Central African Republic, Chad and Equatorial Guinea.

Popular mobilisation against the currency has been intense in recent years in west Africa.

This led to cosmetic changes to the currency arrangements. For example in 2019, French president Emmanuel Macron and the sitting president of Côte d’Ivoire, Alassane Ouattara, announced the withdrawal of French staff from some of the regional central bank’s decision-making bodies. They also waived the requirement – much maligned on the continent – to store 50% of all reserves in Paris as a guarantee to the former colonial power that they wouldn’t be wasted on irresponsible fiscal expansion.

Overall, however, the CFA franc has remained more or less the same and France has not been willing to leave the arrangement of its own accord. The old colonial attachment and supposed developmental benevolence has carried the day.

But the conditions for major change are in place. The Alliance of Sahel States between the junta-led governments of Mali, Burkina Faso and Niger has stated its intention to introduce the “Sahel” as a new regional currency. Whether this initiative – and the Senegalese plan for a national currency – will amount to a full break-up of the CFA franc zone and its terminal decline will depend on how well they plan and execute the transition to several new currencies or a new one without any French involvement.

A hard road ahead

Historically, as shown by Fanny Pigeaud and Ndongo Sylla in their book Africa’s Last Colonial Currency: The CFA Franc Story, serious attempts at leaving the CFA franc since its inception in 1948 have been sabotaged by France.

For example, Guinea was flooded by counterfeit banknotes when it left the CFA franc in the 1960s.

Mali was put under pressure to rejoin the CFA franc after its departure in 1967. It returned into the fold in 1984. In 2011, Ivorian president Laurent Gbagbo, who had been considering pulling out of the CFA franc, was made to step down after controversial elections with the help of a military intervention force. He was then sent to the International Criminal Court before being acquitted 10 years later.

France went further in 2011 – a case countries wanting to make the next attempt at leaving the CFA franc should be cognisant of. It used its seat on the Central Bank of West African States decision-making bodies to block Côte d’Ivoire from being refinanced by the bank.

It also induced the subsidiaries of BNP Paribas and Societe Generale to temporarily close their branches.

Leaving the CFA franc has thus historically come with a high risk of French sabotage.

But the constellation of forces has shifted and west African governments can better prepare this time. If they join forces – and Côte d’Ivoire votes for a less France-dependent president in the presidential elections in 2025 – the end of the west African CFA franc may indeed be near.

The trust factor

The stability and legitimacy of a currency depend primarily on trust. The users of a currency (people and corporations) need to trust that its price is more or less stable. This includes a reasonably low rate of inflation, and engagement in growth-inducing economic activity. Periods of high inflation and hyper inflation have always been the result of a serious economic crisis in which trust was absent.

Monetary stability thus depends on social and macroeconomic stability. This, in turn, is the result of how well governmental policies and domestic and world market processes align. A government that is seen to have a plan and is able to adapt to and steer economic pressure goes a long way in creating trust. And, by implication, it makes a new currency less prone to speculative attack or massive devaluation.

In Senegal, Pastef’s election programme had a roadmap towards leaving the CFA franc and setting up a national currency. Among the key steps are:

- creating a national central bank

- refinancing of state expenditure at 0%

- demonetising gold and preventing its import and export to build up a gold reserve

- repatriating gold reserves still stored in Paris and all over the world

- reprofiling public debt and cancelling private debt through monetary fiat

- installing a deposit insurance scheme for small savers

- building a national stock exchange.

Finally, the new currency will be floating and non-convertible or semi-convertible to shield it from speculative attacks.

This menu is similar to some of the strategies China has employed over the last decades to maintain government control over the economy and shield the Chinese economic growth path from foreign – in other words speculative – interference.

The success of such a strategy depends to a large degree on mobilising domestic financial and real domestic resources. And, in the absence of China’s massive domestic market, building regional economic complementarities.

The strategic challenge for Diomaye will thus be to enlist a sufficiently large group of small business people, landowners and power-brokers around Mouride and Tidjaniyya Muslim brotherhoods and the capitalist class in Senegal to his economically transformative project.

This will be a sizeable challenge in the face of upcoming export revenues from gas and oil – contracts Pastef has vowed to renegotiate – and an overall economic structure that is not yet domestic market oriented.

A national currency could support this shift in focus towards the well-being of the Senegalese people. This is because its logic would be to reorient the government towards the domestic economy and its people. Imports and easy repatriation of earnings by foreign corporations, which are some of the main effects of the often overvalued CFA franc, would become more difficult.

Make or break factors

The reaction to Faye’s agenda by the International Monetary Fund, the World Bank and other donors and creditors will be crucial to watch. To what extent the new Senegalese government is prepared to dispense with their sizeable sums in aid and credits remains to be seen. Niger recently did dispense with them and reduced its budget by 40% as aid was frozen.

Overall, Senegal and the Sahel governments are in a stronger position globally than ever before. The African continent is seen as essential to ensure the energy transition in Europe as well as its diversification of oil and gas supply. And western military, diplomatic and trade hegemony on the continent is being challenged by China and Russia as well as the United Arab Emirates, Qatar and Turkey.

If Senegal and the Sahel governments position the end of the CFA franc well in their overall negotiations with their international partners as well as their domestic capitalist class and opposing political forces, its end may indeed by near.

That will not be the end of the long road towards food, energy and overall economic sovereignty to the benefit of the people. But it will be an important symbolic and material victory against postcolonial interference and meddling.

The colonial CFA franc has outlived its usefulness for today’s “Left Panafricanism”.

Organising its end is a sizeable challenge, but for the first time in decades is one that can be confronted head on.

-

Ghanaian and Senegalese entrepreneurs to benefit from African Development Bank Youth Entrepreneurship and Innovation Multi-Donor Trust Fund (YEI MDTF) grant for green jobs in natural resources

ABIDJAN, Ivory Coast, April 8, 2024/ — The African Development Bank (www.AfDB.org), through its Youth Entrepreneurship and Innovation Multi-Donor Trust Fund (YEI MDTF) (https://apo-opa.co/3J81Cnx), has approved a $999,000 grant to support an initiative to foster green jobs for women, youth and people with disabilities.

The Strengthening Women, Youth and People with Disabilities’ Micro-Entrepreneurship for Green Jobs (https://apo-opa.co/

3U9MFqb) in Natural Resources (MicroGREEN) project aims to foster inclusive economic growth by providing up to 500 green job opportunities and business development services to marginalized groups in Ghana and Senegal. The target reach group includes women, youth and people with disabilities/special needs, engaged in managing natural resource sectors such as agroforestry, fisheries and biodiversity.

The MicroGreen project, to be implemented over two years, will empower with entrepreneurship capacities and business skills at least 1,000 youth aged 15-35 years with female youth-led (60%) , people with disabilities/special needs ( 10%) and other youth (30%) in both countries.

By focusing on capacity building and utilizing value chain-based SME development models, the project endeavors to enhance employment creation, ensure the sustainability of micro-enterprises, and integrate beneficiaries into the economic systems.

Implemented by Invest in Africa (www.InvestinAfrica.com

), a non-profit organization dedicated to fostering African SME growth and creating prosperous economies across the continent, the MicroGREEN project will leverage its expertise in market access, skills development, and access to finance to drive sustainable business growth and job creation in Ghana and Senegal. The African Development Bank founded the Youth Entrepreneurship and Innovation Multi-Donor Trust Fund in 2017 to promote innovation and entrepreneurship as well as to create durable and sustainable jobs for youth on the continent. The trust fund provides grants to support the Bank’s Jobs for Youth in Africa Strategy (https://apo-opa.co/

43RFw2b) programs and initiatives. The Jobs for Youth in Africa Strategy aims to create 25 million jobs and equip 50 million youth with employable and entrepreneurial skills by 2025. Distributed by APO Group on behalf of African Development Bank Group (AfDB).Media contact:

Amba Mpoke-Bigg

Communication and External Relations Department

Email: media@afdb.orgTechnical Contact:

Salimata SOUMARE

Senior Natural Resources Governance Officer

African Natural Resources Management and Investment Centre

Email: s.soumare@afdb.org -

Affirmative Finance Action for Women in Africa (AFAWA) Finance Series Togo: African Development Bank and African Guarantee Fund unite to strengthen female entrepreneurs’ access to finance

LOMÉ, Togo, April 8, 2024/ — The African Development Bank (www.AfDB.org) and the African Guarantee Fund (AGF) (https://apo-opa.co/4apZNya) have brought the curtain down on the AFAWA Finance Series Togo conference, a key note event aimed at promoting a better understanding of the financing needs of Togolese women entrepreneurs and debunking the myth that women-run companies are risky ventures.

The three-day event, which ended on Thursday 28 March 2024, brought together some 180 leading figures responsible for policy and regulation in favour of women’s financial inclusion, and representatives of financial institutions, small and medium-sized enterprises and business incubators run or owned by women.

Specific training was provided to about 30 Togolese financial institutions. The courses helped to enhance understanding of the Affirmative Finance Action for Women in Africa (AFAWA) (https://apo-opa.co/4cPI8Sg) initiative and its ‘guarantee’ mechanism, and demonstrated the commercial benefits of doing a better job of targeting women entrepreneurs by developing gender-sensitive ranges of products and services.

The objective was to better understand the needs of women entrepreneurs and collectively address the challenges they face in terms of access to funding, while exploring the opportunities offered by the Guarantee for Growth programme, designed by the African Development Bank Group through the AFAWA, and implemented by the AGF.

This innovative programme aims to make up to $3 billion available for women-led small and medium-sized enterprises, via guarantees to financial institutions to mitigate lending risks.

Wilfried Abiola, the Bank’s Country Manager for Togo, explained the initiative challenged economic and social stereotypes.

“The AFAWA initiative is not just a financial instrument; it aims to change the narrative and general perceptions, to transform the notion that small and medium-sized enterprises run by women are risky businesses. AFAWA is working to turn these businesses into substantial investment opportunities for institutions, in particular through the Guarantee for Growth programme, which was designed by the Bank,” he declared.

According to Jules Ngankam, CEO of the AGF, “AFAWA also aims to bring together financial and public sector actors to boost human and financial capital so that women can attain their full potential and participate completely in the growth of our continent. We are extremely optimistic that the impact will be significant in the long term and will stimulate economic growth in Togo.”

The financing gap for women-led small and medium-sized enterprises in Togo is close to $45 million. Closing this gap represents a priority for the Togolese authorities, who intend to strengthen women’s economic empowerment, boost the private sector and thereby support inclusive economic growth.

“Through the government’s action, 25 percent of public contracts are now awarded to women and young people, and on the economic front, the government aims to resolve the problem of access to credit for women and girls with the establishment of the National Fund for Inclusive Finance, which has helped more than 1.2 million women,” said Koffi Gani, Principal Private Secretary for the Togolese Minister for Social Action, the Advancement of Women and Literacy.

The AFAWA Finance Series Togo conference is part of a series of events organised right across Africa to promote access to finance for businesses run or owned by women. It represents a considerable step towards accomplishing the ambitious goal of funding women-led businesses to the tune of $5 billion by 2026.

The African Development Bank, through the AFAWA initiative, has approved approximately $1.7 billion in cumulative investments and $54.5 million in technical assistance, and has partnered with 96 financial institutions in 32 regional member countries. Over 7,000 women-led small and medium-sized enterprises have now reaped the benefits of its support in Africa.

AFAWA is supported by the Women Enterpreneurs Finance Initiative (We-Fi), the G7 countries of France, Italy, Canada and Germany, as well as the Netherlands and Sweden.

Distributed by APO Group on behalf of African Development Bank Group (AfDB).Media contact:

Désirée Bataba

Communication and External Relations Department

media@afdb.org -

Africa Finance Corporation’s year of impact sees major expansion of projects and investment

LAGOS, Nigeria, April 8, 2024/ — Africa Finance Corporation (AFC) (www.AfricaFC.org), Africa’s leading infrastructure solutions provider, has announced its most impactful year to date, with unprecedented expansion of projects and investments spanning energy, transportation, mining, food, textiles and climate resilience.

Underpinning robust growth in earnings and total assets, AFC successfully navigating the global geopolitical, inflationary and debt distress challenges of 2023 to implement critical infrastructure projects across multiple sectors that are central to Africa’s structural transformation and sustainable development.

Landmark initiatives include Djibouti’s first wind farm, with AFC as lead developer advancing plans to become the first African country wholly reliant on renewable sources for energy, and the Lobito Corridor rail project, with AFC again as lead developer working alongside the US, European Union and governments of Angola, DRC and Zambia to mobilise industry and connect the Atlantic and Indian oceans. Advancing industrialisation, value creation and livelihoods,

AFC with its partner Arise IIP expanded the Arise Special Economic Zones to 10 West and Central African countries, focusing on essential sectors including food security, textiles and minerals.

“At the heart of AFC’s mission is our commitment to deliver impactful solutions for Africa, and this guides each and every investment we undertake,” said Samaila Zubairu, AFC’s President and CEO. “AFC’s impact is evident in our solutions-oriented approach and unwavering commitment to realising transformative projects across Africa—infrastructure projects like the Red Sea Power Wind Farm in Djibouti, the Arise IIP industrial zones and the Lobito transport corridor that are reshaping the landscape, fostering sustainable development for local communities, and altering the economic trajectory of countries.”

Created through powerful international collaborations, AFC projects undertaken in 2023 also include a joint initiative with Xcalibur Multiphysics to advance the mapping and responsible utilisation of Africa’s natural mineral resources, enabling greater mineral beneficiation, diversified economies, and clean energy transition.

In DRC, the Corporation has committed to helping overhaul Kinshasa’s mass transit system to enhance mobility and reduce pollution through a partnership with Trans Connexion Congo.

A historic commitment of US$253 million from the Green Climate Fund to the AFC Capital Partners’ Infrastructure Climate Resilient Fund (ICRF) marked a significant step toward developing sustainable, climate-resilient infrastructure in Africa.

Each initiative blends meaningful development impact and environmental sustainability with strong risk-adjusted returns, leveraging AFC’s unique experience of de-risking project development to crowd in capital and accelerate completion.

“In a year marked by global economic and geopolitical complexities, AFC has stood as a beacon of resilience, delivering value to all stakeholders while creating jobs and prosperity through structural transformation across Africa,” said Mr. Zubairu. “Our robust financial results reflect AFC’s unwavering commitment to unlock practical solutions for projects that enhance local value capture and spur industrialisation.”

AFC’s annual profit rose 15.3% to US$329.7 million, while operating income increased 24.2% to US$497.5 million, and total assets expanded 17.3% to US$12.34 billion, surpassing the Corporation’s 5-year strategy target by US$2.3 billion.

Further significant financial highlights include:

- Return on average equity at 11.0% (2022: 12.1%)

- Net interest income up 31.3% to US$430.5 million (2022: US$327.9 million)

- Total comprehensive income up 14.6% to US$327.0 million (2022: US$285.3 million)

- Capital adequacy ratio increased to 34.5% (2022: 34.3%)

AFC’s high-profile exit from the Atlantic Terminal Port in Takoradi, Ghana, through a sale to major global ports operator Yilport exemplified strategic divestment.

The Corporation expanded its presence with three new member states—Ethiopia, Burundi, São Tomé and Príncipe—bringing the total to 43. Six new sovereign shareholders were also onboarded, including Turk Eximbank becoming the first non-African shareholder. Equity investments in addition from the governments of Côte d’Ivoire, Benin and Botswana, Cameroon’s Caisse Nationale de Prévoyance Sociale (CNPS), and SBM Capital Market Securities Ltd. in Mauritius helped increase AFC’s total equity by 26.7% to US$3.42 billion.

Debt market transactions further broadened AFC’s investor base with significant global financial institutions participating in a record US$625 million syndicated loan, supported by a 62% oversubscription. The Corporation also received a US$350 million line of credit from the African Development Bank and a €50 million facility from Cassa Depositi e Prestiti, showcasing the Corporation’s ability to attract regional and international institutions.

“As AFC charts its course to further elevate our impact across the continent, we remain deeply appreciative of the unwavering support of our stakeholders and the dedication of our team, whose passion drives our mission forward,” said Mr. Zubairu. “With a refreshed strategic agenda emphasizing balanced portfolio growth, innovative financing, and enhanced operational capacity, AFC is well-positioned to shape a robust future for African infrastructure and development.”

Distributed by APO Group on behalf of Africa Finance Corporation (AFC).Media Enquiries:

Yewande Thorpe

Communications

Africa Finance Corporation

Mobile : +234 1 279 9654

Email : yewande.thorpe@africafc.org -

President Ramkalawan announces the appointment of women professionals in key positions

To coincide with the International Women’s Day, the President of the Republic, Mr Wavel Ramkalawan has recently appointed four women professionals in prominent positions in the administration of the country.

These are:

The re-appointment of the Governor of the Central Bank of Seychelles, Ms Caroline Abel, the new Principal Secretary for Finance, Ms Astride Tamatave, the new Commissioner General of the Seychelles Revenue Commission (SRC) Mrs Varsha Singh, and also the appointment of the Chief Executive Officer of the National Bureau of Statistics, Mrs Li Fa Cheung Kai Suet.

Governor of the Centrel Bank, Ms Caroline Abel – Ms. Caroline Abel was first appointed Governor of the Central Bank of Seychelles (CBS) on 14th March 2012, becoming the first woman in Seychelles to hold the position. She was re-appointed to serve a second six-year term in March 2018.

Principal Secretary for Finance, Ms Astride Tamatave – Ms Tamatave is a certified Chartered Accountant with ACCA Professional Qualification (equivalent to MSC). She also holds a Master’s Degree in Leadership & Strategy in the Social Domain from the Institute of Public Administration.

She has 16 years of working experience in the private sector and the public service in the domain of accounting and finance. She previously held the position of Comptroller General.

Commissioner General of the Seychelles Revenue Commission (SRC) Mrs Varsha Singh – Mrs Singh, a South African national, has over 28 years experience in tax, customs, transfer pricing, trade facilitation, international relations, and building organisational excellence and driving sustainable development.

She holds a Masters Degree in International Customs Law and Administration from the University of Canberra, Australia, as well as a Masters in Business Administration from the Management School of Southern Africa, South Africa.

Chief Executive Officer of the National Bureau of Statistics, Mrs Li Fa Cheung Kai Suet – Mrs Li Fa Cheung Kai Suet served for 10 years as the Director/Chief Executive Officer of the National Statistics Agency (Statistics Mauritius), prior to which she has previously served in various key positions such as Deputy Director and Senior Economist at the International Monetary Fund (IMF).

In conveying his sincere congratulations to the women professionals President Ramkalawan said “This is a sign of the confidence that our administration has in the ability of women to participate in the development of Seychelles.

I wish them all the very best in their responsibilities ahead. I have no doubt that they will deliver to the best of their abilities and make Seychelles proud as they contribute in the economic development of the country.

SOURCE

State House News Alert

Office of the President of the Republic of Seychelles

-

African Development Bank launches historic 10.5-year inaugural USD Global Sustainable Hybrid transaction

ABIDJAN, Ivory Coast, February 1, 2024/ — The African Development Bank (www.AfDB.org), rated Aaa/AAA/AAA/AAA (Moody’s/S&P/Fitch/Japan Credit Rating, all stable) has successfully launched and priced its first Sustainable US dollar-denominated 750 million perpetual subordinated hybrid capital notes.On the 30th of January 2024 the African Development Bank launched a hybrid capital transaction with a coupon of 5.75% until August 2034, with a 10.5 year first call date at the Bank’s discretion. The Bank achieved a top quality and granular orderbook with over 275 investors, of which over 190 were allocated. Investor demand was very strong with a peak orderbook of over USD 6 billion.

The largest share of the allocation was taken up by Hedge / Specialised funds (54.8%), followed by Asset Managers (27.8%), Central Banks and Official Institutions (6.7%), Pension Funds / Insurance (6.6%) and Banks / Private Banks (4.1%). Demand came mainly from the UK (51.1%), followed by EMEA (26.5%), Asia (14%) and Americas (8.4%).

This is the first sustainable hybrid capital issuance by a multilateral development bank, marking the African Development Bank’s pioneering role in optimizing its balance sheet in line with the G20 Capital Adequacy Framework (CAF) recommendations to boost lending capacity. Hybrid capital is an innovative form of capital which increases sustainable lending capacity.

The Bank mandated BNP Paribas and Goldman Sachs International as Joint Structuring Agents and Barclays, BNP Paris, BofA Securities and Goldman Sachs International as Joint Bookrunners to lead manage its new Perpetual Non-call (PerpNC) 10.5-year inaugural USD Global SEC-exempt Sustainable Hybrid transaction.

African Development Bank Vice President for Finance and Chief Financial Officer Hassatou N’Sele said the move followed close monitoring of the market since the institution’s roadshow last September, to generate interest in the bond.

“This landmark transaction was received with marked enthusiasm by a broad range of investors. It paves the way for the African Development Bank and other AAA-rated Multilateral Development Banks to further leverage their capital base and increase their support to Africa and the developing world, who are facing multiple crises and long-term development challenges, in a context of constrained development resources.”

Omar Sefiani, Bank Group Treasurer said: “We saw tremendous interest from over 275 investors resulting in a record order book for the AfDB. The outstanding success of this transaction allows the African Development Bank to demonstrate that MDBs can tap the private investor market to supplement their capital base and therefore allow incremental sustainable lending to their clients.”

African Development Bank celebrates a decade of ESG Bond issuances

Monday’s transaction marks a decade of bond issuance in the Environmental, Social and Governance (ESG) space for the pan-African lender.

The notes will be issued in a Sustainable Bond format, under the Bank’s 2023 Sustainable Bond Framework and will be leveraged through new green or social bonds. As a new component of the African Development Bank’s capital base, the Sustainable Hybrid capital will allow additional lending capacity to fund environmental and/or social projects.

In 2013 the African Development Bank issued its inaugural green bond, listed on the Luxembourg Stock Exchange (LuxSE). It has been issuing social bonds since 2017. The new Sustainable Bond Program, established in 2023, combines and updates the previous Green Bond Program and Social Bond Program, enabling the issuance of green bonds, social bonds, and sustainability bonds. These ESG bonds contribute to the fight against climate change and reinforce socio-economic development in the Bank’s Regional Member Countries.

On January 22, the African Development Bank launched and priced a USD 2 billion 3-year Social Global Benchmark due 25 February 2027, its first global benchmark of the year. The 3-year social bond, issued under its new Sustainable Bond Framework established in September 2023, further consolidates and enhances the Bank’s existing Green and Social Bond programs.

For more details on the transaction click here (https://apo-opa.co/4bjpLEe).

Distributed by APO Group on behalf of African Development Bank Group (AfDB) -

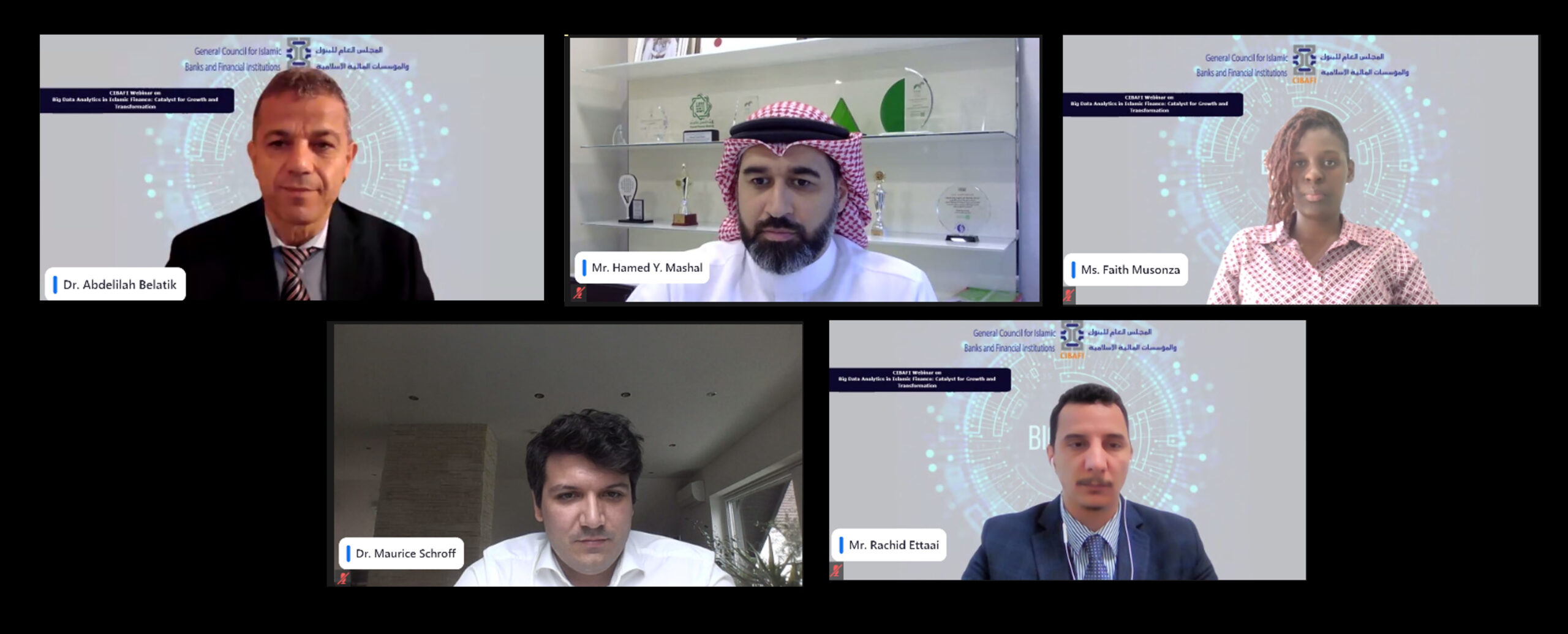

The Catalytic Role of Big Data Analytics in Shaping Islamic Finance Underscored

Story: Mohammed A. Abu

A webinar held by the General Council for Islamic Banks & Financial Institutions(CIBAFI) concluded with a forward-looking perspective on the future of big data and its transformative potential in the Islamic financial industry, underscoring its role as a catalyst for growth and transformation, an official statement said in Manama, Bahrain, Tuesday.

CIBAFI’s Secretary General, Dr. Abdelilah Belatik, in his inaugural address, it said, underscored the critical significance of big data in Islamic finance emphasizing that, it goes beyond mere technological advancement and it is a strategic imperative as well.

Dr. Belatik highlighted its transformative impact, empowering financial institutions with actionable insights, facilitating problem-solving, fostering innovation, and supporting informed decision-making aligned with Islamic principles.

Held under the theme, “Big Data Analytics in Islamic Finance: Catalyst for Growth and Transformation”. the webinar gathered industry experts to explore the dynamic intersection of big data and the financial sector with a focus on Islamic finance

A panel session moderated by Mr. Rachid Ettaai, Business Development Manager, CIBAFI.featured industry experts who discussed key aspects of big data analytics, including its influence on financial products, emerging trends, and strategies for data-driven innovations.

They tackled challenges related to privacy, skills, and infrastructure, emphasizing ethical considerations in data processing. The speakers’ insights enriched the discussion, providing a comprehensive view of big data’s transformative potential in Islamic finance.

The panelists included Mr. Hamed Y. Mashal, Executive Manager – Head of Retail Banking, Kuwait Finance House – Bahrain and the Chairman of CIBAFI Information and Technology Working Group (ITWG); Ms. Faith Musonza, Strategy and Digital Financial Inclusion Expert, Acuma, United Emirates; and Dr. Maurice Schroff, Principal at Strategy&, Germany.

SOURCE

CIBAFI

-

The African Development Bank plans to invest USD 10.5 million in the capital of Seedstars Africa Ventures to boost investment in innovative businesses

ABIDJAN, Ivory Coast, January 18, 2024/ — The Board of Directors of the African Development Bank (AfDB) (www.AfDB.org) agreed on Wednesday that the Bank should take a stake of USD 10.50 million in the capital of Seedstars Africa Ventures S.L.P. venture capital fund to enable it to invest in innovative African businesses with strong growth potential.

The Bank agreed to invest USD 7 million from its ordinary resources and USD 3.5 million from the European Union Boost Africa programme. The investment will allow Seedstars Africa Ventures (SAV) to raise funds, expand its presence in Africa and attract other investors.

Seedstars Africa Ventures is an early-stage venture capital fund investing in high-growth companies active across Sub-Saharan Africa.

The fund focuses on businesses that have strong potential, are generating income and tackling key challenges in the market. It mainly targets sub-Saharan Africa, especially markets less well covered by traditional investors, and enjoys a particular focus on French-speaking countries such as Senegal, Côte d’Ivoire, Benin and Cameroon. However, it also has investments in Ghana, Uganda and Tanzania.

As a venture capital fund of USD 75 million, Seedstars Africa Ventures targets the start-up and launch phases of businesses tackling key constraints in the market. Initial investments are around the EUR 250,000 mark, followed by additional capital injections of €5 million to support their growth.

SAV focuses on financial inclusion and the technologies that equip businesses (fintech and insurtech); retail sales and logistics platforms that target the online and mobile consumers market; health-related technologies; pre-paid, off-grid energy; and more generally, the adoption of technology in businesses, particularly in the food-processing industry and value chains.

It is estimated that the fund will help create 9,000 full-time jobs, 50% of them for women, and have a significant economic impact.

The fund’s objectives are in line with those of Boost Africa, which aims to invest in innovative start-ups that are growing strongly and having a positive social impact.

Its investment strategy will strengthen that of the African Development Bank, which links entrepreneurship, investment and economic growth to poverty reduction and sustainable development.

It will also contribute to the Bank’s operational priorities – the High 5 – by supporting start-ups operating in key sectors, such as agriculture, health, industrialization and off-grid energy. Finally, the investments will contribute to strengthening regional integration and improving the lives of people in Africa.

Distributed by APO Group on behalf of African Development Bank Group (AfDB).Media contact:

Romaric Ollo Hien

Communication and External Relations Department

African Development Bank

media@afdb.org